The Article 9 process is the framework under the Uniform Commercial Code (UCC) that governs what happens when a business defaults on secured debt. “Secured” means the loan or advance is backed by a lien on your business assets, recorded through a UCC-1 filing. Article 9 sets out what a creditor may do to recover, and what protections you keep as the debtor.

At its core, the process gives a secured creditor the right to take possession of the pledged collateral after a default and dispose of it to satisfy the debt. In exchange, the debtor gets procedural safeguards: advance written notice of any sale, a requirement that the sale be commercially reasonable, and an accounting of the proceeds. The trigger for everything that follows is a single event — default, as defined in your loan or security agreement.

Because the framework is detailed but leaves room for negotiation, the same rules that let a lender enforce also let both sides settle on modified terms without a sale. That flexibility is why the Article 9 process, far from being purely a repossession tool, is so often the vehicle for a cooperative restructuring. If a UCC-1 lien has been filed against your business, you are already inside the world Article 9 governs.

Whether it ends in a sale or a negotiated restructuring, the Article 9 process moves through the same defined stages. Knowing each one tells you where you are and where you still have leverage.

There is a seventh possibility that never appears on this list because it interrupts it: negotiation. At almost any point before a disposition, the debtor and secured creditor can agree to modified terms — a restructured payment schedule, a new security arrangement, or acceptance of the collateral in satisfaction of the debt (§9-620). This negotiated off-ramp is where restructuring lives, and for a business worth more running than closed, it is almost always the better outcome for everyone at the table.

The Article 9 sale process is the disposition stage above, seen in full. It is how a secured creditor converts collateral into cash to satisfy a defaulted debt — and it is bounded by two hard requirements.

First, notice. The creditor must send reasonable authenticated notification before the sale, to the debtor and to certain other parties with an interest in the collateral (§9-611). Skip or botch that notice and the sale can be challenged. Second, commercial reasonableness. Under §9-610, a low price alone is not the test, but every aspect of how the sale is conducted must be commercially reasonable — a lender cannot dump assets in a way engineered to leave a large deficiency. Because an Article 9 sale is not supervised by a court, questions of process and price are examined after the fact, which is exactly why a careful creditor keeps the sale defensible.

When the sale completes, it transfers to the buyer all of the debtor’s rights in the collateral and discharges the security interest and any subordinate liens (§9-617). The secured party typically provides only minimal representations and warranties. Proceeds pay the sale costs, then the debt; a shortfall leaves a deficiency, and a surplus, when it exists, goes back to the debtor. For a distressed owner, the sale is the outcome to avoid — and the notice window is often the last moment when a negotiated alternative is still on the table.

Article 9 exists to standardize how secured transactions work across every state. Before the Uniform Commercial Code, a lender taking collateral in one state could face entirely different rules in the next; Article 9 replaced that patchwork with one coherent framework, adopted in all 50 states (Louisiana has ratified it only in part).

Practically, Article 9 governs the full life cycle of a security interest: its creation (called attachment), its perfection (usually by filing a UCC-1 financing statement), its priority when more than one creditor claims the same collateral, and its enforcement after default. It applies to security interests in personal property and fixtures — equipment, inventory, receivables, and the like — not to real estate, which is governed by separate state law. The purpose throughout is predictability: lenders extend secured credit when they know their rights, and borrowers benefit both from that available credit and from knowing, in advance, what a default sets in motion. The full statute is published by the Legal Information Institute at Cornell Law School.

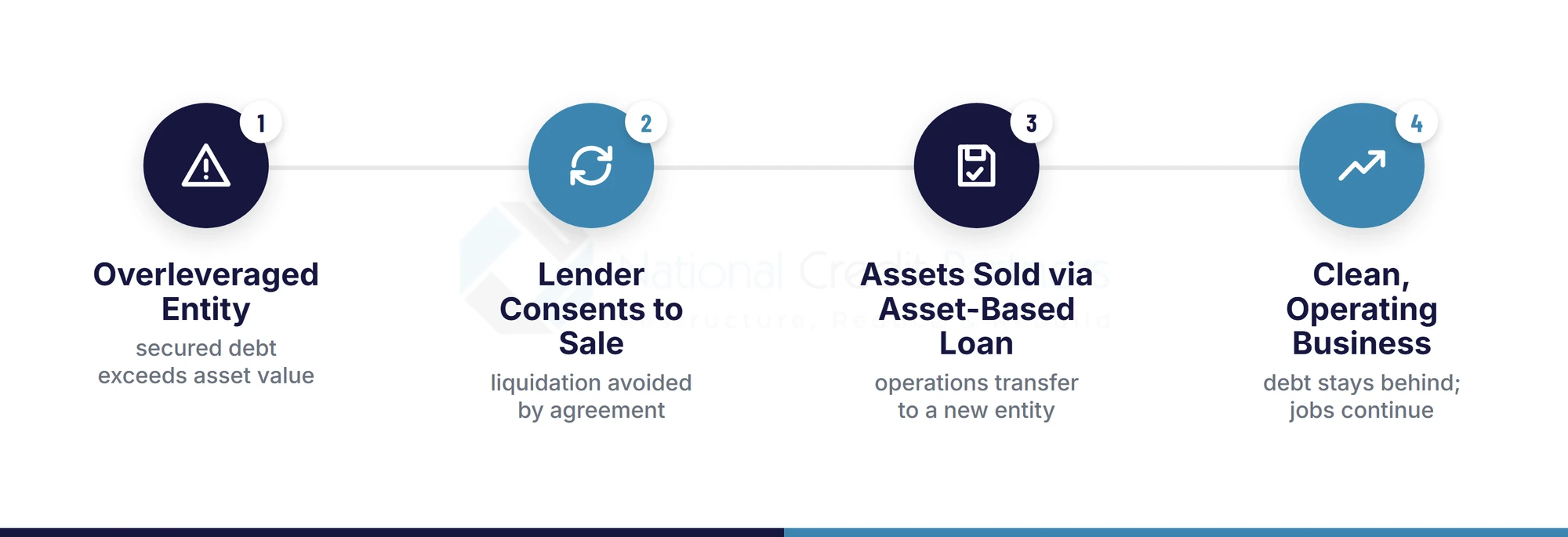

An Article 9 reorganization is the cooperative version of everything above. Instead of an adversarial sale that ends the business, the debtor and secured lender use the same disposition mechanism to preserve it. It is best understood as a controlled sale of the business’s assets that maximizes value for everyone involved — because when a business simply shuts down, every party recovers less.

Here is how it works in practice. With the business owner’s consent, the secured lender elects not to liquidate the collateral at auction but to sell the operating assets into a new, separate business entity — a transfer usually financed by an asset-based loan. The new entity starts with a clean balance sheet: the operations and assets carry over, but the crushing debt of the old entity does not. The business keeps running, employees keep their jobs, and the owner keeps the ability to earn.

This is why a bank will, counter-intuitively, cooperate in a process that removes debt. Liquidation is a last resort: auctioning used business assets recovers little, takes time, and costs money, and the recovery value is uncertain. A preserved, operating business can keep producing value and ultimately return more than a dead one ever could. Business press has described Article 9 reorganizations as among the quickest and least expensive ways to resolve a company whose debts far exceed the value of its assets — a genuine alternative to bankruptcy rather than a step toward it.

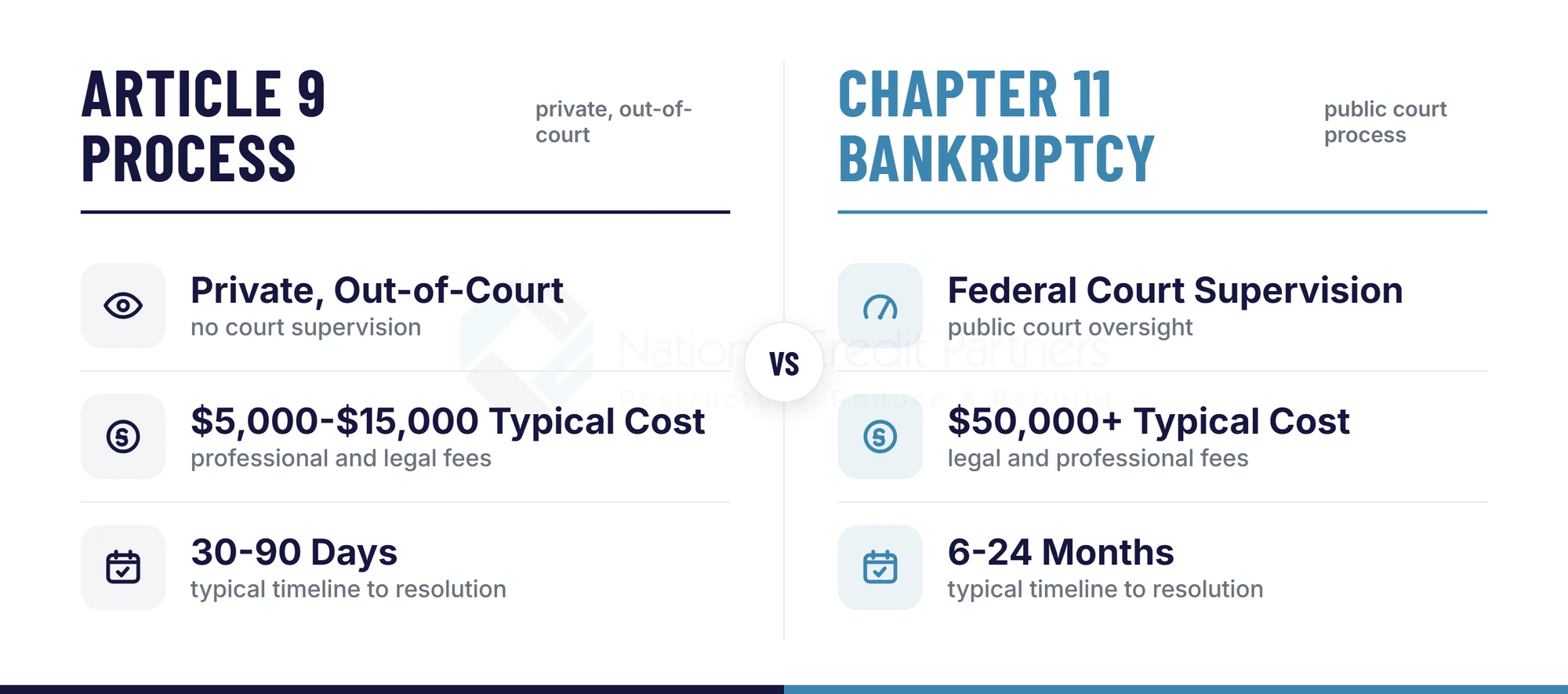

The most common question distressed owners ask is how the Article 9 process compares to filing Chapter 11. The short answer: Article 9 is private, faster, and far cheaper, and it keeps you out of court.

| Factor | Article 9 process | Chapter 11 bankruptcy |

|---|---|---|

| Court involvement | Private, out-of-court negotiation | Federal court supervision |

| Typical cost | Roughly $5,000–$15,000 | $50,000+ in legal and professional fees |

| Typical timeline | 30–90 days | 6–24 months |

| Public record | Private | Public court filing |

| Business operations | Continue throughout | Continue, but under court oversight |

| Typical outcome for SMBs | Negotiated resolution; business preserved | Difficult for SMBs; can convert to Chapter 7 liquidation |

The cost and speed gap matters most for smaller companies. Chapter 11 was built for large enterprises with the time and cash to fund a lengthy reorganization, and it is widely regarded as slow and costly for a small business. Completing a reorganization plan is difficult, and some cases convert to Chapter 7 liquidation instead. Congress created Subchapter V to make small-business bankruptcy lighter and faster, and it can be the right tool for some. But it is still a public court process. The Article 9 process remains the out-of-court route: private, quicker to resolve, and structured to keep the business operating.

A typical Article 9 restructuring runs 30 to 90 days from the first consultation to a finalized agreement. The exact timeline depends on how many creditors are involved and how complex the debt structure is. A single-creditor case can close in as little as 30 days; a multi-creditor restructuring with stacked positions usually takes the full 90. Set against the 6-to-24-month arc of a Chapter 11 case, the difference is not marginal — it is the difference between resolving a cash-flow crisis and running out of runway during it.

The Article 9 process applies to businesses with secured debt — debt where a UCC-1 financing statement has been filed against the company’s assets. If your financing is backed by that kind of lien, it is in scope.

Qualifying debt types include merchant cash advances, equipment loans, secured business lines of credit, SBA-guaranteed loans, and bank loans secured against business assets. Merchant cash advance debt is the most common trigger we see — especially where several advances have been stacked against the same receivables and daily or weekly ACH debits have overwhelmed cash flow.

What does not qualify is unsecured debt. Trade credit with no UCC filing, business credit cards, and similar obligations fall outside Article 9 and call for a different approach entirely. The dividing line is always the lien: no security interest, no Article 9.

The Article 9 process does affect business credit, but typically less severely than bankruptcy, because it is a private negotiation rather than a public court record. How much impact depends on how each lender reports the resolved account and on the specific terms agreed.

This is where the outcome you negotiate matters most. National Credit Partners works to ensure advances are shown as “paid in full” rather than “settled for less” wherever possible — protecting the business’s standing with future lenders and keeping the door open to traditional financing down the road. The label attached to a resolved account can shape your access to credit long after the debt itself is gone.

Most owners do not run the Article 9 process alone, and they should not have to. This is where debt-relief firms come in — but it is worth being precise about what different firms actually do, because the category is not uniform.

As a category, debt-relief firms take a range of approaches. Some negotiate with secured creditors to reduce the principal owed or to settle the debt at a discount; others focus on extending the payment term or restructuring the underlying security interest. Approaches that reduce or settle principal can lower a balance, but they can also leave a resolved account marked “settled for less” — a flag that future lenders notice.

National Credit Partners’ approach is deliberately different. We do not describe our work as debt settlement, and we do not aim to have your accounts marked as settled. Our model is structured reconciliation: we negotiate directly with secured creditors to modify the terms of the advance — the schedule, the structure, the arrangement — with the goal of resolving the debt in full rather than settling it for less. The distinction is not cosmetic. It is the difference between a business that closes its Article 9 matter in good standing with lenders and one that carries a settlement flag into its next financing application.

National Credit Partners specializes in helping small and mid-sized businesses resolve secured debt through the Article 9 process — negotiating a mutually beneficial agreement that can put a business on a workable, restructured footing in as little as 30 days. Two things set the approach apart:

We have helped businesses in default, in collections, facing legal action, and contending with stacked MCA positions work back toward traditional financing — SBA loans or term loans — after coming through the process. Our A+ rating with the Better Business Bureau reflects that record. If your business is carrying $50,000 or more in secured debt and the daily or weekly debits have become unmanageable, the earliest conversation is the most valuable one: the sooner the Article 9 process is handled deliberately, the more options stay open.

Talk through your Article 9 options with a structured reconciliation specialist. The consultation is free, and taking the first step is often where the pressure starts to lift.

Get a Free ConsultationThe Article 9 process is not something that happens to a business so much as something a business can steer. Left alone, it runs toward a sale — notice, disposition, discharge. Engaged early, that same framework becomes the fastest private route to a restructured, operating company that keeps its people and its standing with lenders. Knowing which stage you are in, and where the negotiated off-ramp sits, is what turns a default notice into a decision rather than an ending.

What is an article 9 process?

The Article 9 process is the set of rules under the Uniform Commercial Code that governs what a secured creditor may do after a business defaults on collateralized debt. It permits the creditor to take possession of the pledged collateral and dispose of it to satisfy the debt, while giving the debtor procedural protections such as advance notice and a commercial-reasonableness standard on any sale. In practice, the same framework also lets the two sides negotiate a modified, out-of-court arrangement instead of a forced sale.

What is the Article 9 sale process?

An Article 9 sale is the disposition of a defaulting debtor’s collateral under UCC §9-610. The secured party must send reasonable advance notice (§9-611) and conduct the sale — public or private — in a commercially reasonable manner. A completed sale transfers the debtor’s rights in the collateral to the buyer and discharges the security interest and any subordinate liens (§9-617). Proceeds are applied to the costs of sale and then the secured debt, with any surplus returned to the debtor or any deficiency remaining owed.

What is the purpose of article 9?

Article 9 standardizes how secured transactions work across all 50 states. It governs the creation (attachment), perfection, priority, and enforcement of a creditor’s security interest in a debtor’s personal property and fixtures — the collateral behind loans, bonds, and advances. The goal is a predictable, uniform framework so lenders can extend secured credit and both borrowers and creditors know their rights if a default occurs.

What is an article 9 reorganization?

An Article 9 reorganization is a cooperative, out-of-court restructuring that uses the Article 9 disposition process to preserve a business rather than liquidate it. With the debtor’s consent, the secured lender sells the business’s assets into a new, debt-free operating entity — often financed by an asset-based loan — so operations, jobs, and value continue instead of being lost at auction. It is designed to leave creditors better off than they would be in a shutdown.

An A+ rating represents BBB's high degree of confidence that the business is operating in a trustworthy manner and will make a good faith effort to resolve any customer concerns filed with the BBB.